Introduction

Every investor who has ever lost a significant amount of money made the same fundamental error before the loss happened. They focused entirely on potential gains and gave inadequate thought to potential losses.

Risk management is not a defensive strategy reserved for cautious or timid investors. It is the core discipline that separates investors who survive and compound wealth over decades from those who experience one catastrophic loss that sets them back years.

Warren Buffett's two famous rules of investing are both about risk. Rule one: never lose money. Rule two: never forget rule one.

This guide covers the essential principles of risk management that apply whether you are investing in stocks ETFs cryptocurrencies or trading forex. These are not advanced concepts reserved for professional fund managers. They are foundational principles every investor should understand and apply from their very first trade.

What is Investment Risk?

Risk in investing refers to the possibility that an investment will produce a return different from the one expected. This includes the possibility of losing some or all of the money invested.

Risk is not synonymous with loss. Risk is uncertainty. A high risk investment does not always produce a loss. A low risk investment does not always produce a gain. Risk describes the range of possible outcomes and the probability distribution across those outcomes.

There are two main categories of risk that investors encounter.

Systematic risk also called market risk is the risk that affects all investments simultaneously. A global recession affects nearly every stock. A sharp rise in interest rates affects both stocks and bonds. A pandemic disrupts all markets. Systematic risk cannot be diversified away by holding more assets because all assets tend to move together during systemic events.

Unsystematic risk also called specific risk is the risk associated with a particular company sector or asset. The risk that a pharmaceutical company fails its drug trial. The risk that a specific country's currency devalues due to political instability. The risk that a cryptocurrency project is exposed as fraudulent. Unsystematic risk can be reduced through diversification because it is unlikely that all positions in a portfolio will experience the same specific negative event simultaneously.

Understanding which type of risk you are facing is the starting point for managing it effectively.

The 1% Rule and Position Sizing

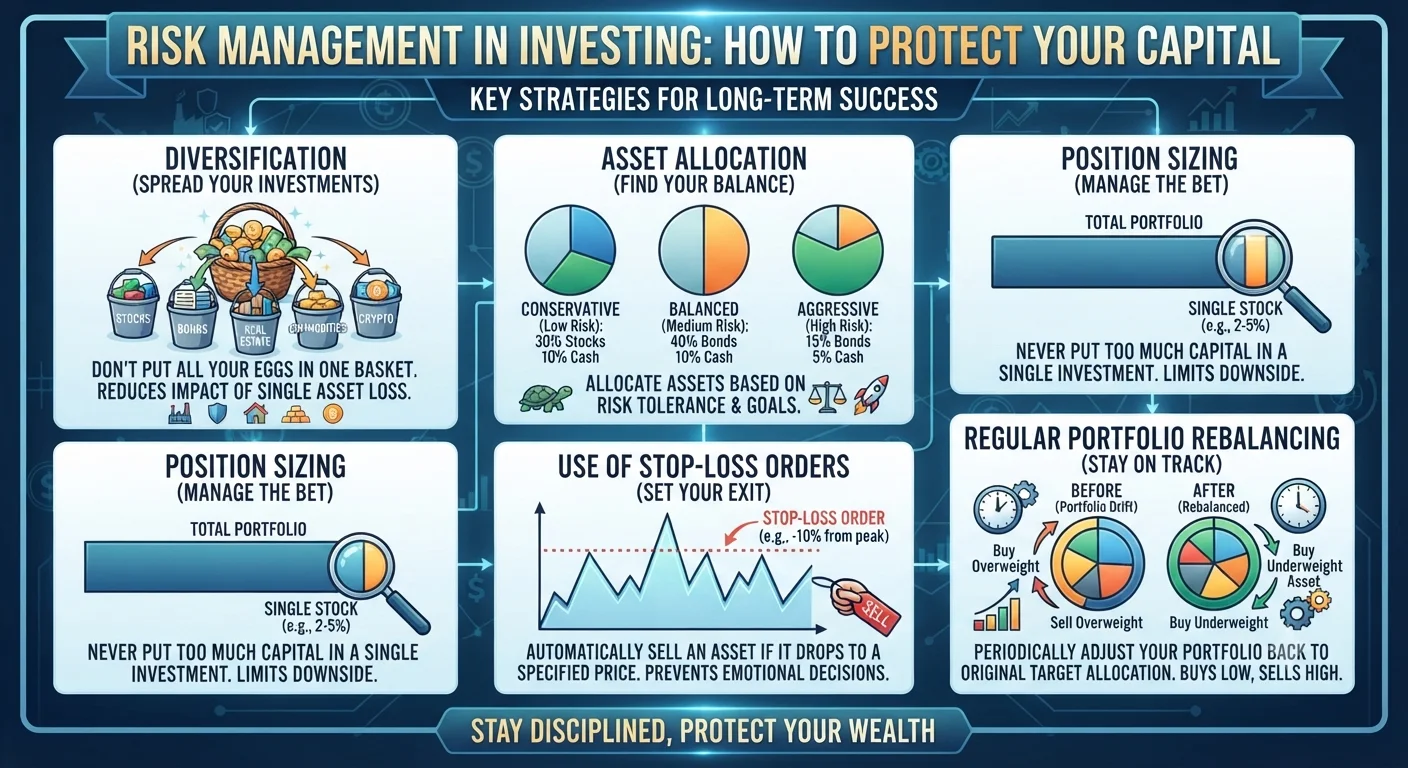

Position sizing is the practice of determining how much of your total capital to allocate to any single investment or trade. It is perhaps the single most important risk management tool available to retail investors.

The 1% rule states that you should never risk more than 1% of your total account on any single trade. If your account is worth ten thousand dollars your maximum loss on any single trade should be one hundred dollars.

This rule exists because it makes you mathematically resilient to losing streaks. If you risk 1% per trade you can lose 20 consecutive trades and still retain approximately 82% of your starting capital. You can continue operating. You have time to learn from mistakes and adjust your approach.

By contrast if you risk 10% per trade you can be eliminated in just 10 consecutive losses. This can happen to even skilled traders during unfavourable market conditions.

Position sizing in practice works like this. You decide in advance where your stop loss will be on a trade. The stop loss is the price level at which you will exit if the trade moves against you. The distance from your entry price to your stop loss price determines the size of position you can take while keeping your risk within the 1% limit.

For investors rather than active traders the same principle applies in modified form. Concentrating a large percentage of your portfolio in a single stock or cryptocurrency is the equivalent of risking too much on one outcome. A position that represents more than 5 to 10 percent of your total portfolio creates significant dependency on the performance of that single holding.

Diversification: The Only Free Lunch in Finance

Nobel Prize winning economist Harry Markowitz described diversification as the only free lunch in finance. The idea is that combining assets whose returns are not perfectly correlated reduces the overall risk of a portfolio without necessarily reducing the expected return.

If you hold only one stock and that stock falls 60% your portfolio is down 60%. If you hold 20 stocks and one of them falls 60% your portfolio is down approximately 3% assuming the other 19 remain flat. Diversification across multiple positions absorbs the shock of any single failure.

Effective diversification means more than just holding many different assets. True diversification requires that those assets have low correlation with each other. Correlation measures how closely the price movements of two assets track each other. Assets with high positive correlation tend to rise and fall together which defeats the purpose of diversification.

Holding both Bitcoin and Ethereum provides much less diversification than it appears because the two cryptocurrencies have historically shown very high correlation. They tend to rise and fall at approximately the same times and for approximately the same reasons.

A better diversified portfolio might combine domestic equities with international equities with bonds with real estate investment trusts and perhaps a small allocation to commodities like gold. These asset classes have historically shown lower correlations with each other particularly during non crisis periods.

The important limit of diversification is that it cannot eliminate systematic risk. When global markets fall sharply in a crisis most assets fall together regardless of how many different positions are held. Diversification protects against specific risks not against broad market panics.

Stop Losses and Take Profit Levels

A stop loss is an instruction to exit a trade automatically when the price reaches a predetermined level. Setting a stop loss before entering a trade is one of the most basic and most frequently violated rules of risk management.

Many beginners avoid stop losses because they do not want to accept a loss. The irony is that refusing to use a stop loss leads to much larger losses. A trade not stopped out at a 2% loss has a habit of becoming a 10% loss then a 20% loss as the investor convinces themselves the position will recover.

Stop loss placement should not be arbitrary. Placing it too close to your entry means being stopped out by normal price fluctuation before the trade has time to develop. Placing it too far away means the potential loss exceeds your risk parameters.

There are several logical approaches to stop loss placement. Technical traders place stops just beyond significant support or resistance levels. Volatility based traders use the Average True Range indicator to set stops at a distance that accounts for the normal daily fluctuation of the asset. The key principle is that your stop loss should be placed at a level where being stopped out means your original trade thesis was wrong. Not that the market moved against you temporarily.

A take profit level is the price at which you plan to exit a trade with a gain. Defining your take profit level before entering a trade allows you to calculate your risk to reward ratio. If your potential loss to your stop loss is 100 dollars and your potential gain to your take profit level is 300 dollars your risk to reward ratio is 1:3. A 1:2 ratio is generally considered the minimum acceptable for most trading strategies because it means you can be wrong more than half the time and still generate positive returns overall.

Psychological Risk: The Trader's Hidden Enemy

All of the risk management tools described above are mechanical. They work when applied correctly. The challenge is that human psychology creates powerful impulses that lead investors to abandon their rules at exactly the moments when following them matters most.

Fear and greed are the two dominant emotional forces in investing. Greed causes investors to take oversized positions in assets that have already risen significantly. This is chasing past performance rather than future probability. Fear causes investors to sell at exactly the worst time during market panics when long term fundamentals have not changed.

Overconfidence is particularly dangerous after a period of success. A winning streak leads many investors to believe they have developed a skill that does not yet exist. They increase position sizes. They take on more risk. When the inevitable loss arrives it is disproportionately large relative to their account.

Confirmation bias leads investors to seek out information that supports their existing positions and ignore information that contradicts them. A trader who is long Bitcoin will tend to read bullish analysis and dismiss bearish analysis not because the bullish arguments are stronger but because they feel more comfortable.

Revenge trading is the impulse to immediately re enter the market after a loss with a larger position in order to recover the lost money quickly. It is one of the fastest ways to turn a manageable loss into an account destroying series of losses.

The antidote to all of these psychological pitfalls is a written trading plan with clear rules for position sizing entry and exit and a commitment to reviewing adherence to those rules rather than simply reviewing profit and loss figures.

Systematic vs Unsystematic Risk in Practice

Understanding the difference between these two risk types changes how you build a portfolio in practice.

Systematic risk cannot be avoided through asset selection. The way professional investors manage it is through asset allocation adjustments based on market cycle stage. During late cycle economic conditions with tight monetary policy many institutions reduce equity exposure and increase cash or short duration bond holdings. This is not market timing in the speculative sense. It is a structural risk reduction response to changing macro conditions.

Unsystematic risk is managed through diversification across individual positions industries geographies and asset classes. A portfolio concentrated in one sector is exposed to sector specific downturns that a diversified portfolio would absorb more comfortably.

For most retail investors the practical implication is straightforward. Keep individual position sizes small relative to the total portfolio. Spread exposure across multiple uncorrelated assets. And never allocate so much to a single position that being wrong about it would fundamentally damage your financial situation.

Conclusion

Risk management is not the opposite of making money in investing. It is the prerequisite for making money sustainably over time. Every investor who has built lasting wealth understood one thing more deeply than anything else: protecting capital is more important than maximising any individual return.

The 1% rule keeps individual losses small enough to survive. Diversification spreads exposure across uncorrelated risks. Stop losses enforce discipline when psychology urges you to hold on. Understanding your own psychological tendencies is the ongoing work of every honest investor regardless of experience level.

Start with these principles before you start with strategy. Strategy without risk management is speculation. Risk management is what turns speculation into investing.

Disclaimer: This article is for educational and informational purposes only. It does not constitute financial or investment advice. All investing involves risk including potential loss of principal. Always conduct your own research and consider seeking advice from a qualified financial professional before investing.

Related Articles: What is Forex Trading? A Beginner's Complete Guide for 2026 What Moves Forex and Crypto Prices? Global Market Drivers Explained How to Start Investing with $100: A Practical 2026 Guide